Business News

Huge Update: Courts Vacate the FCC's One-to-One Consent Rule

What does it mean for the Life Insurance Industry?

Written by: Paul Bloodsworth

February 14, 2025

[5 minute read]

Indroduction

Just 2.5 days before the One-to-One Consent Rule was set to take effect, the U.S. Court of Appeals for the 11th Circuit vacated the FCC’s revised interpretation of “prior express written consent.” This ruling is a game-changer for life insurance carriers, agents, and lead generators who rely on consumer data to drive business and sales.

What does this mean for the life insurance and lead generation industries? Are you in the clear, or is there still risk?

We cover this in the video below:

The 11th Circuit Court Vacates the One-to-Once Consent Rule.

Who petitioned? and

What now for life insurance agents and lead generators?

Why Was the One-to-One Consent Rule Challenged?

The Insurance Marketing Coalition (IMC) filed a petition to halt the rule, arguing that businesses—especially small insurance agencies—did not have enough time to adjust their operations to comply by the January 26th deadline.

But let’s be real—who stood to lose the most? Big lead-selling companies like Integrity and other members of the of IMC. These companies profit from selling a single consumer’s data multiple times over the years. If the One-to-One Consent Rule had taken effect, it would have forced lead sellers to change their entire business model, directly affecting the way life insurance agents access and purchase leads.

Subject to change as further petitioning and new rulings are still being discussed.....

Consumer Complaints and TCPA Violations

Although the One-to-One Consent Rule was vacated, other compliance requirements still exist:

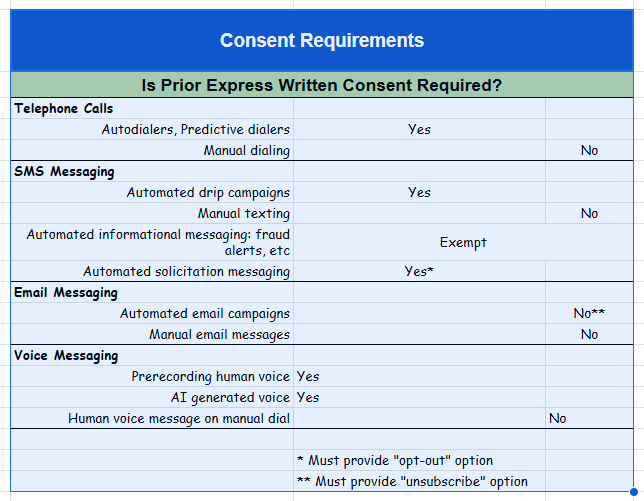

✅ Life insurance agents must still obtain consent before using automated dialers, AI voices, or prerecorded messages.

✅ Aged leads can still be sold—for now.

✅ Lead generators must disclose who they are when obtaining consent.

✅ Manual dialing remains permissible, as long as the number is not on the Do Not Call (DNC) list.

How did we get here? The History of Prior Express Consent

The Telephone Consumer Protection Act (TCPA) was enacted in 1991. However, it wasn't until 2012 that the FCC clarified the definition of prior express consent before contacting consumers using automated systems. The definition was clear:

“An agreement, in writing, bearing the signature of the person called that clearly authorizes the seller to deliver… advertisements or telemarketing messages using an automatic telephone dialing system or an artificial or prerecorded voice.”

This rule had been quietly in place for years—until December 13, 2023, when the FCC announced an expansion to One-to-One Consent to prevent the resale of leads.

If implemented, this would have prevented lead companies from selling consumer data beyond the first transaction. Naturally, lead-selling giants and insurance marketers fought to keep their revenue model intact, leading to the 11th Circuit’s decision to vacate the rule just days before enforcement.

(Lobbying power and several attorneys...)

What happens next for Life Insurance & Lead Generation?

While this ruling provides some relief, it doesn’t mean the industry is off the hook. The TCPA still applies, and regulators are closely watching how insurance carriers, agents, and lead generators operate.

💡 Next Steps:

- If you rely on leads, ensure you work with reputable lead vendors who follow compliance guidelines.

- If you use auto-dialers, verify you have proper consent documentation.

- Expect more legal challenges and changes in the regulatory landscape.

- Prepare for new compliance measures—this issue is far from over.

And if you’re wondering just how many times a single lead gets resold—stay tuned for our next video, where we use AI to analyze the shocking truth behind lead recycling.

Upcoming Podcast

Let's Get Clarity from a TCPA Attorney

We'll be announcing a date for an upcoming podcast with Eric Troutman. Eric and I recorded a podcast previously, but much has transpired in the interim. We'll be discussing these issues as they pertain specifically to the life insurance industry.

Share your thoughts in the comments section of the videos below!

Additional Resources:

📜 Read the official petition to the court from the IMC

🎧 Listen to our latest podcast

📩 Send us an email requesting to join our exclusive email list. (This is a small, private list. Include in your message which organization you represent.) Email to: marketing@go-excel.com